How Health Insurance Subsidies Actually Work (and Who They Really Help)

Every Open Enrollment season, I get hit with the same handful of questions:

“Do I qualify for a subsidy?”

“Why did my rate go up when my income didn’t?”

“How come my neighbor pays $50 a month and mine’s $600?”

If you’ve ever stared at your Marketplace quote like it’s written in another language, you’re not alone.

So, let’s break down what health insurance subsidies actually are, who qualifies, how much people really get, and what’s changing this year versus next year.

Because this is one of those things that can literally make or break your wallet and misunderstanding it costs people thousands.

🩺 What a Subsidy Actually Is (and Isn’t)

A subsidy is a federal tax credit that lowers your monthly premium when you buy health insurance through the ACA Marketplace (HealthCare.gov or your state exchange).

It’s not a coupon. It’s not charity. It’s a tax credit — meaning you’re getting an advance on money that would’ve gone toward your taxes anyway.

The amount you qualify for depends on two main things:

1️⃣ Your household income (based on Modified Adjusted Gross Income. Number 11 on your taxes.)

2️⃣ The cost of a mid-level “benchmark” Silver plan in your area

The lower your income compared to the cost of coverage in your zip code, the bigger your subsidy.

💡 Example: How Subsidies Work in Real Life

Let’s take two households.

Example 1: Sarah

Age 42

Single, makes $45,000 per year

Lives in Florida

Non-smoker

Her preferred plan costs about $620/month without subsidies.

Based on her income, she’ll get about a $375 subsidy, dropping her monthly cost to around $245.

Example 2: The Johnsons

Married couple, two kids

Combined income: $110,000

Live in Illinois

Their benchmark family plan runs about $1,450/month.

They qualify for a $900 monthly subsidy, paying about $550/month after the credit.

Both are middle-class families who’d never afford coverage without those subsidies.

That’s why this system matters. And why everyone’s watching 2026 like it’s a countdown clock.

⚖️ What’s Changing (and Why It Matters)

Since 2021, the American Rescue Plan Act and Inflation Reduction Act expanded the ACA subsidies so more people qualify and everyone gets a bigger discount.

It removed what’s called the “Subsidy Cliff” — the old rule that cut people off if they earned over 400% of the federal poverty level.

In plain English: before 2021, if you made one dollar too much, you could lose your entire subsidy at tax time.

Between 2021 and 2025, your subsidy simply tapered down as your income rises; so high earners still get some help if insurance premiums take up too much of their income.

But here’s the catch:

That expansion expires at the end of 2025 unless Congress extends it. (Which they are supposed to be voting on in “mid-December,” though the Open Enrollment for January 1st ends December 15th. Talk about 11th hour!)

If it expires, the old rules come back. This means millions of middle-class Americans will wake up in 2026 paying 75–100% higher premiums for the exact same coverage.

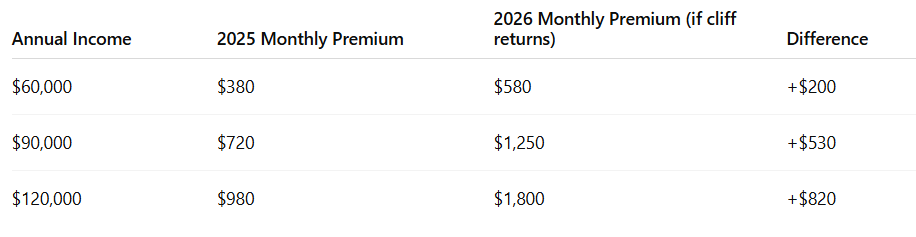

🧮 Example: How the Subsidy Cliff Would Hit Different Incomes

Let’s look at 2025 vs 2026 for a family of four in Georgia.

That’s not a scare tactic. Those are real math projections from the Kaiser Family Foundation.

If Congress doesn’t act, it won’t just hit “wealthy” families. It’ll crush small business owners, freelancers, and anyone earning just above that 400% income mark.

🙋♀️ Who This Doesn’t Affect (At Least for Now)

Let’s clear up a few common questions I get every week:

❓“What if I have insurance through work?”

You’re fine. Employer-sponsored coverage isn’t based on ACA subsidies.

❓“What if I’m on Medicaid or Medicare?”

Not affected at all. Those programs run separately.

❓“What if my spouse has employer coverage but I don’t?”

That depends on the new “family glitch fix.”

If your employer’s plan is unaffordable for the whole family (meaning it costs more than 9.39% of your income), you can qualify for subsidies for your dependents.

❓“What if I’m undocumented?”

ACA subsidies are only available to U.S. citizens and legal residents.

Undocumented immigrants can’t buy Marketplace coverage. Undocumented immigrants have never been able to buy Marketplace coverage. They also cannot qualify for Medicaid or Medicare.

❓“What if I’m paying $0 for my 2025 plan?”

Your plan will probably go up in price. Many people’s have due to the regular increase in price of the ACA plans. However, your subsidies are not in jeopardy. For an individual, you have to make more than about $65k to reach the Subsidy Cliff and your plan would already be more than $0 per month for 2025.

💬 Why Honesty (or Slight Overestimation) Matters

When applying for Marketplace coverage, you estimate your expected income for the upcoming year.

That determines your monthly subsidy.

Here’s where people get into trouble:

If you underestimate and earn more than expected, you might owe back part of your subsidy at tax time.

If you overestimate, you could get a refund.

So, yes — it pays to be cautious.

👉 Insured AF Tip:

Estimate a little high. It’s way more fun to get money back than to owe the IRS in April.

💸 How Much People Usually Get

The average subsidy nationwide right now is around $6,400 per year (or about $530 per month), according to the Centers for Medicare & Medicaid Services (CMS).

But in high-cost states like Florida, Arizona, and Texas, it can reach $800–$1,200 per month for families.

Even people earning over $100,000 still qualify in some areas, depending on their age, county, and plan costs.

That’s why there’s no one-size-fits-all answer. Two families with identical incomes can have totally different subsidies just based on where they live.

🧾 The Biggest Mistake I See

Every year, people get scared by the math and say, “Forget it, I’ll just go uninsured.”

But here’s what they miss:

Even with no subsidy, a private plan or supplemental combo is often cheaper than paying full price for a Marketplace plan.

And if you do qualify — those credits can be the difference between paying $900/month or $300/month.

That’s why reviewing your eligibility each year isn’t optional. Tt’s essential.

⚡ The Insured AF Reality Check

Subsidies are the reason millions of middle-class families can actually afford to stay insured.

But the system isn’t “set it and forget it.”

It changes every year, every income bracket, every zip code.

Don’t assume what worked in 2025 will still work in 2026.

You deserve to know how your plan — and your subsidy — will hit your wallet before the renewal notice shows up.

💥 Call to Action

If you’re not sure whether you qualify for help (or how much), message me.

I’ll run the numbers, show you what’s changing in your area, and help you figure out whether Marketplace, private, or small business coverage makes the most sense.

📘 Grab the book: The Health Insurance Solution — learn the system like a pro.

📓 Use the workbook: The Health Insurance Workbook — fill in your numbers and compare plans with clarity.

This Open Enrollment, be prepared, not panicked.

🧾 TL;DR

Subsidies lower your Marketplace premium — based on income & plan cost.

Expanded subsidies (thanks to ARPA/IRA) are still active through 2025.

If Congress doesn’t act, they expire in 2026 → “The Subsidy Cliff.”

Overestimate income slightly to avoid tax payback later.

Check your eligibility yearly — the difference can be thousands.